By now, almost no one would deny that passive, index-based investment strategies have performed well this decade. Since 2010, passive strategies have managed favorable risk-reward performance by nearly any metric. During this time, U.S. equities and longer-term bonds have helped investors recover from the poor performance that passive strategies had generated the prior decade. The so-called “lost decade” from 2000-2009 was one that included two severe bear markets in which equities twice lost about half of their value, generating a negative return for equities for the decade. By contrast, investors have seen no such trouble since 2010.

But the great divergence between the performance of passive strategies during these two decades should give investors pause before considering whether passive investment strategies will succeed in the next decade. No one investment strategy works all the time, and even the best strategies will not always live up to expectations. So the question arises, how might an investor manage the risk that the same passive strategy that performed so well in the current decade will not perform so well in the next?

One simple method is to incorporate a tried-and-true investment strategy that can be easily implemented into an ordinary 401k or IRA portfolio—momentum. Momentum investing is based on the simple principle that securities that have performed well in the recent past will continue to perform well in the future. The same principle may sound risky or exotic to passive investors, but those who try it may be pleasantly surprised at the degree to which momentum strategies both avoid risk and generate return. This is especially true if momentum strategies are evaluated over a full market cycle, including a full bear market and bull market.

There is a growing body of academic literature on the benefits of momentum investment strategies. Gary Antonacci’s Dual Momentum (2014) and Qualitative Momentum (2016), by Wes Gray and Jack Vogel, are excellent places to start. Antonacci’s websites, http://www.optimalmomentum.com/ and https://www.dualmomentum.net/ provide a wealth of useful information about how investors can utilize a simple momentum strategy with mutual funds or exchange-traded funds (ETFs), among other useful information.

One way of demonstrating whether momentum investing is effective would be to determine how a portfolio would have performed in this decade if a simple momentum strategy had been combined with a simple passive strategy. First, consider the performance of a passive, “lazy” portfolio consisting of mutual funds or ETFs rebalanced annually. Notably, these portfolios are similar to the target-date retirement funds held by many 401k plans and which are the default investment option for many 401k investors. There are many such “lazy portfolios” that can be found through the internet, and Paul B. Farrell provides performance data on several such portfolios on his Marketwatch page: https://www.marketwatch.com/lazyportfolio.

One “lazy” portfolio, created by famed investor Peter Bernstein, contains simply four positions in equal sizes. Bernstein’s portfolio consists of:

(1) an ETF for U.S. stocks, specifically an S&P500 index fund (ticker: SPY);

(2) an ETF for foreign stocks (EFA);

(3) an ETF for U.S. small-cap stocks (IWM); and

(4) an ETF for a long-term bond index (IEF).

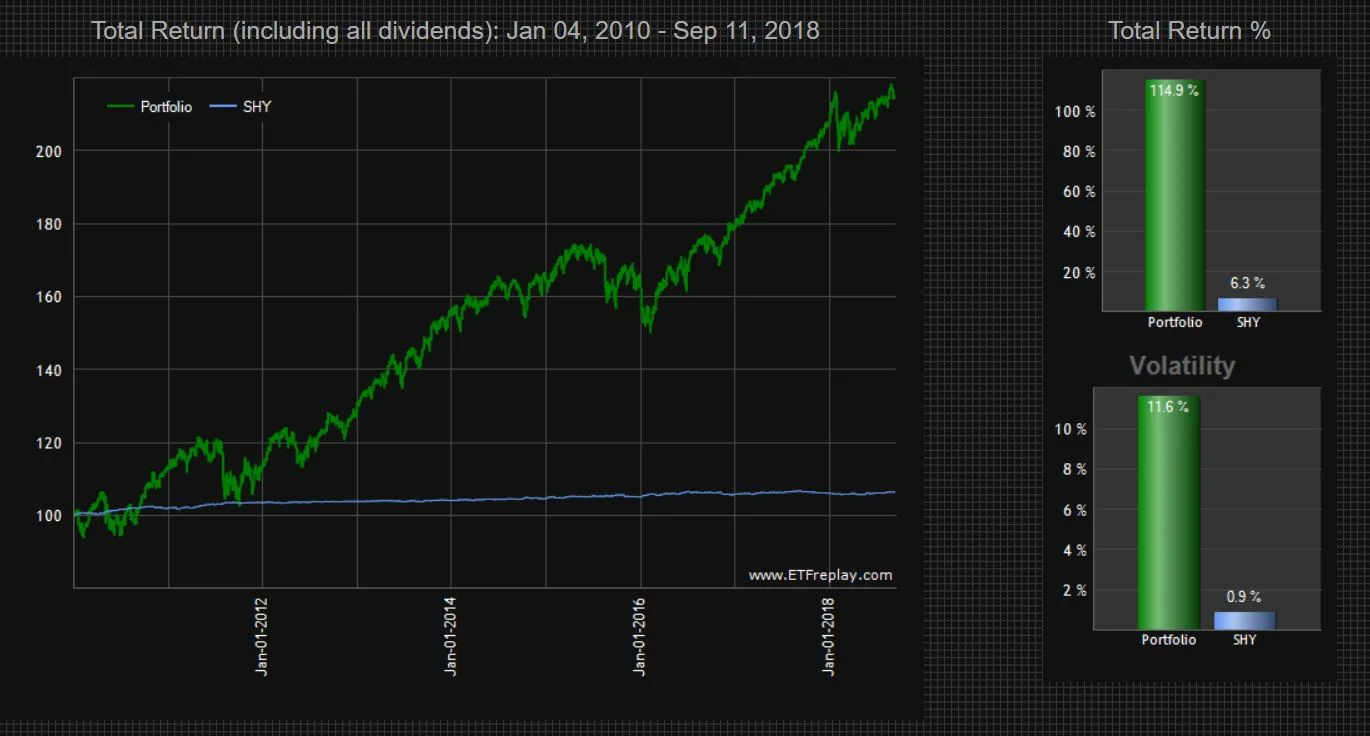

If you invested in these four funds in equal amounts on the first trading day of January 2010, and rebalanced the portfolio each year to equalize the size of the positions, your portfolio would have generated the following results compared to holding short-term U.S. bonds throughout the period (ticker: SHY).

Chart graphics courtesy of ETFreplay.com. Results are hypothetical, are NOT an indicator of future results, and do NOT represent returns that any investor actually attained. Results are unmanaged and do not reflect management or trading fees.

Bernstein’s portfolio would have enabled an investor to collect a significant benefit from the bull market in equities this decade, while mitigating some of the volatility generated by equities with the generic bond index position. The compound annual growth rate (CAGR) for Bernstein’s strategy was 9.2%, while holding short-term bonds would have generated a CAGR of only 0.7%. Investors would have more than doubled their money this decade with a simple and easily implemented investment strategy. Nor would investors have needed to suffer through any major “drawdowns,” or the biggest percentage decline from a portfolio high. In this regard, Bernstein’s portfolio suffered a worst drawdown of only 15.3%, which occurred in 2011.

While Bernstein’s strategy manages to illustrate well the benefits of passive investing in index funds, it’s worth pointing out that there is nothing magical about Bernstein’s strategy as opposed to some other index-based strategy. Many of these strategies are almost interchangeable. This is the conclusion reached by Meb Faber in his Global Asset Allocation (2015).

But what if the buy-and-hold investor had decided to split the portfolio into equal halves, one half containing Bernstein’s portfolio and one half containing a momentum strategy based on Bernstein’s portfolio? The results may surprise passive investors.

First, what are the rules of this momentum strategy? Instead of buying and holding the four positions and rebalancing them annually, each quarter we select the top two performing positions over the prior quarter and invest the momentum half of this portfolio in equal amounts in these two positions for the next quarter and repeat each quarter. This way we emphasize the stronger aspects of the Bernstein portfolio on a quarterly basis.

Also, we want to protect capital in case these top performers are in a downtrend regardless of their performance relative to the other funds. So, if the price of the top performing funds is weak over the prior quarter, we want to hold AGG, the generic bond index fund, in place of the top performing fund. It won’t help us if the top performers are not performing well on an absolute basis, even if they are performing better relative to the other funds in the portfolio.

Significantly, the results for the combined portfolio show a higher annualized return than for the passive portfolio, 10.4% versus 9.4%. But was the combined portfolio difficult to follow with high volatility? No, in fact, it was easier to follow. The volatility for the portfolio containing momentum was lower than for the passive, buy-and-hold portfolio, 10.7% versus 11.6%. Also, the maximum drawdown with the combined portfolio was lower than for the passive portfolio 13.9% versus 15.3%. Finally, if you visually compare the “equity curves” of the two charts, the line moving from the lower left to the upper right, you will notice that the equity curve for the second chart is smoother, making for better portfolio performance overall.

Chart graphics courtesy of ETFreplay.com. Results are hypothetical, are NOT an indicator of future results, and do NOT represent returns that any investor actually attained. Results are unmanaged and do not reflect management or trading fees.

The price of such benefits likely amounts to less than an additional 60 minutes of portfolio management per year. Instead of rebalancing annually, the portfolio is rebalanced quarterly with few trades. Nor does it increase costs because most brokers include commission-free ETF options that are compatible with this strategy. But even if this approach is too difficult for the passive investor, hiring an investment advisor to rebalance the portfolio quarterly for a reasonable fee (0.50 to 1.25% annually), while the adviser provides behavioral coaching and other financial advice, would be an intelligent decision as well.

No one knows how passive investors will fare in the next decade, but incorporating a simple momentum strategy is one straightforward way they can manage the risk that the next decade will not be as kind as the current one.